I want to tell you the story of one of the biggest impacts I ever made. I’m going to assume that you don’t know much managerial accounting. That’s fine; I didn’t either when I started this project. I’m going to give you a five minute tutorial on managerial accounting in this post. Your goal is to understand how to calculate contribution margin per unit and why it’s important. Then I’ll get to my story.

Our problem

Our company sells tree, shrub, and berry seedlings online. Before we did any managerial accounting we carried a few hundred different species and ages of trees. We knew that we made a profit overall at the end of the year because our financial accounting showed a profit for the whole business. But we had only a fuzzy idea how much profit we were making on each product individually.

We were largely in the dark on many important details such as:

- how profitable are our products?

- which products are the most profitable? least profitable?

- are we selling any products at a loss?

- which customers are most profitable? least profitable?

- which segments of our market are the most profitable? least profitable?

- are our products priced correctly? what would happen if we raised the price 20% or lowered it by 10%?

- if we find ourselves overstocked what price change should we make to generate the most profit?

- if we only have room to grow another 10,000 trees, which species and ages should we grow to maximize profit?

- how can we increase the profitability of our business?

I did some research and found out that managerial accounting had the answers to all our questions (or at least a method to help us figure it out).

Why should a programmer like you care about managerial accounting?

Managerial accounting can help managers make smart decisions about the direction of their company. But in our company–and I suspect many companies–we didn’t have any way to do any managerial accounting calculations. All our detailed sales data was in our web database but all our receipts and accounting data was stored in a completely separate system. The business people understood the power of managerial accounting but lacked the computer skills to do the actual calculations.

And that’s where 10x programmers come in. They see the value of the calculations and jump at the chance to learn how to slice and dice the data and do the calculations required to calculate contribution margin.

If your company isn’t doing any kind of managerial accounting, introducing it could be a game changer–it sure was for us. Plus, I’m only giving you the tiniest introduction to the potential of managerial accounting. It’s a huge area with many excellent ideas for an aspiring 10x programmer.

Let’s get some definitions and calculations out of the way and then I’ll continue my story.

What is managerial accounting

Managerial accounting is a system of accounting used to help managers make better decisions within their organizations. This is a separate discipline with different goals than financial accounting (with its famous income statements and balance sheets).

What is contribution margin

Contribution margin is the selling price per unit minus the variable cost per unit. “Contribution” represents the portion of sales revenue that is not consumed by variable costs and so contributes to the coverage of fixed costs.

How to calculate contribution margin

Contribution Margin is the money left over from sales after you subtract your variable costs.

The easiest way to understand contribution margin is with a simple example. Suppose you had a lemonade stand and you sold 1,000 glasses of lemonade at $1/glass. The lemonade cost you $200 and your glasses cost $100.

Contribution margin = selling price – the sum of all incremental and avoidable costs (in this simplified case they are your lemonade and glasses).

$700 = ($1 x 1,000) – ($200 + 100)

Once you have your contribution margin, it’s easy to calculate your overall profit if you know your unavoidable and sunk costs (in this simplified case these are your fixed costs).

Fixed costs:

- lemonade stand: $200

- advertising: $100

- sunscreen: $25

Fixed costs = $325

Profit = contribution margin – fixed costs

$375 = $700 – $325

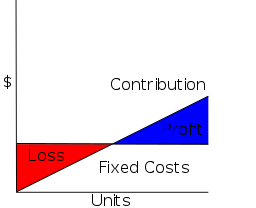

How to calculate contribution margin per unit

Break-even point for contribution margin

Contribution margin per unit = Contribution margin / number of units sold

$0.70 = $700 / 1,000

Each glass of lemonade you sell adds $0.70 to our contribution margin. The contribution margin on your first glasses of lemonade is used to cover your fixed costs.

At some point you reach your break-even point, after which all the contribution margin you make is profit. I’ll leave it to you to calculate the break-even point on your lemonade stand.

Why does contribution margin per unit matter?

Once you calculate contribution margin per unit, you can easily compute:

- your break-even point for each product (the number of sales required to cover all fixed costs)

- projected profit for a given sales forecast

- which of your products are most profitable (if you calculate the contribution margin per unit for all the products you sell individually)

- the relationship between changes in selling price and profit (how many more units you have to sell to break even on a price drop or how many fewer units you need to sell to break even on a price increase)

You can use this information to make informed decisions about your product mix, marketing strategy, and pricing strategy. This information gives you an advantage over competitors making these decisions based on historical data and guess work.

Conclusion

Thanks for hanging in there. I know this post was a little dry. But I promise it was both necessary and worth the effort to give you the background required to appreciate the story of one of the biggest impacts I ever made. Stay tuned.

0 Comments

1 Pingback